CITY OF GLASGOW COLLEGE / MERGER PROPOSAL DOCUMENT

23

SECTION 6: Supporting Evidence Base

6.3 Financial Benefi ts

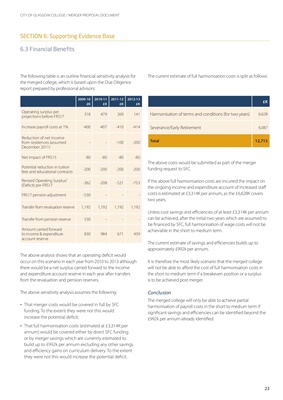

The following table is an outline i nancial sensitivity analysis for

the merged college, which is based upon the Due Diligence

report prepared by professional advisors:

The above analysis shows that an operating dei cit would

occur on this scenario in each year from 2010 to 2013 although

there would be a net surplus carried forward to the income

and expenditure account reserve in each year after transfers

from the revaluation and pension reserves.

The above sensitivity analysis assumes the following:

That merger costs would be covered in full by SFC

funding. To the extent they were not this would

increase the potential dei cit;

That full harmonisation costs (estimated at £3,314K per

annum) would be covered either by direct SFC funding

or by merger savings which are currently estimated to

build up to £992k per annum excluding any other savings

and ei ciency gains on curriculum delivery. To the extent

they were not this would increase the potential dei cit.

•

•

The current estimate of full harmonisation costs is split as follows:

The above costs would be submitted as part of the merger

funding request to SFC.

If the above full harmonisation costs are incurred the impact on

the ongoing income and expenditure account of increased staf

costs is estimated at £3,314K per annum, as the £6,628K covers

two years.

Unless cost savings and ei ciencies of at least £3,314K per annum

can be achieved, after the initial two years which are assumed to

be i nanced by SFC, full harmonisation of wage costs will not be

achievable in the short to medium term.

The current estimate of savings and ei ciencies builds up to

approximately £992k per annum.

It is therefore the most likely scenario that the merged college

will not be able to af ord the cost of full harmonisation costs in

the short to medium term if a breakeven position or a surplus

is to be achieved post merger.

Conclusion

The merged college will only be able to achieve partial

harmonisation of payroll costs in the short to medium term if

signii cant savings and ei ciencies can be identii ed beyond the

£992k per annum already identii ed.

£K

Harmonisation of terms and conditions (for two years) 6,628

Severance/Early Retirement 6,087

Total 12,715

2009-10

£K

2010-11

£K

2011-12

£K

2012-13

£K

Operating surplus per

projections before FRS17

318 479 269 141

Increase payroll costs at 1% -400 -407 -410 -414

Reduction of net income

from residences (assumed

December 2011)

- - -100 -200

Net impact of FRS15 -80 -80 -80 -80

Potential reduction in tuition

fees and educational contracts

-200 -200 -200 -200

Revised Operating Surplus/

(Dei cit) pre-FRS17

-362 -208 -521 -753

FRS17 pension adjustment -530 - - Transfer

from revaluation reserve 1,192 1,192 1,192 1,192

Transfer from pension reserve 530 - - Amount carried

forward

to income & expenditure

account reserve

830 984 671 439